Apple is pressing down further on its financial services offerings, with a new savings account offering on top of Apple Card. The move, as is the case with most new Apple launches, has created ripples in the fintech industry, with many speculating about the potential implications and impact on the financial services landscape.

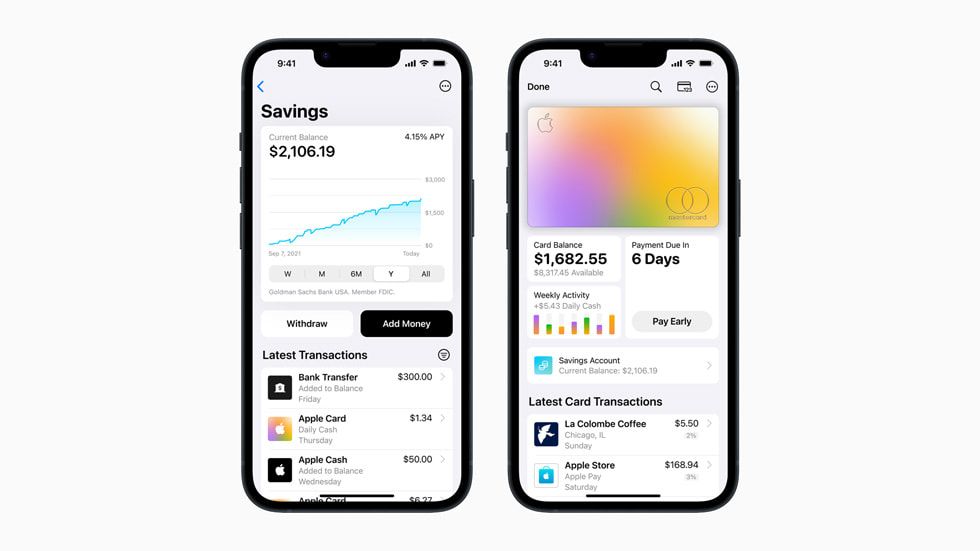

In an official release, Apple announced that Apple Card users in the US can now open a high-yield savings account to grow their Daily Cash rewards. The account offers a high-yield APY of 4.15%, which is more than 10 times the national average, Apple noted. This development is hardly unexpected, given that Apple had originally announced it back in October, but at that time, the company said that it was unable to share what interest rate would be paid out on these accounts due to the fluctuating nature of rates.

The interest rate offered by Apple is among many high-yield savings accounts offered by other companies. In fact, the Federal Deposit Insurance Corporation notes that the national average APY on savings accounts is just 0.35%. Apple’s entry into the savings account market comes as part of its ongoing efforts to diversify its revenue streams beyond hardware and software products. In pursuit of this new financial product, Apple has teamed up with Goldman Sachs to offer the savings account. The company noted that the Daily Cash rewards earned by customers through the Apple Card will automatically be deposited to the savings account. Customers will have the ability to change where their Daily Cash is deposited at any time, as well as the ability to add funds from their own bank accounts to the savings account at any time.

The high-yield interest rate is something that is sure to attract attention from consumers who seek better returns on their savings in a low-interest rate environment. Not only does it challenge traditional banks by offering a compelling alternative to traditional savings accounts, with higher interest rates and a user-friendly digital experience, but it could also prompt other financial institutions to reevaluate their offerings and strive to provide similar features to remain competitive. Furthermore, the development could also impact existing fintech companies that offer similar services. While Apple has the advantage of its large customer base and brand recognition, smaller fintech players may face increased competition and pressure to differentiate themselves in the market.

“Savings helps our users get even more value out of their favorite Apple Card benefit — Daily Cash — while providing them with an easy way to save money every day,” Jennifer Bailey, Apple’s vice president of Apple Pay and Apple Wallet, said in an official statement. “Our goal is to build tools that help users lead healthier financial lives, and building Savings into Apple Card in Wallet enables them to spend, send, and save Daily Cash directly and seamlessly — all from one place.”

Apple’s move into financial services also highlights the increasing convergence of technology and finance, which has been a growing trend in recent years. This blurring of lines between industries is likely to accelerate as tech companies with vast user bases and advanced technological capabilities, such as Apple, enter the financial services arena.

And the best thing about the new savings account is that it does not burn a hole in your pockets at all. There are no fees involved in the creation of the account, nor are there any minimum deposits or minimum balance requirements. However, there is a maximum balance limit on the savings account – $250,000. Users can directly set up and manage the accounts directly from the Apple Card in the Apple Wallet on their iPhones.

The Tech Portal is published by Blue Box Media Private Limited. Our investors have no influence over our reporting. Read our full Ownership and Funding Disclosure →

Soumyadeep is a Reporter at The Tech Portal, reporting on startups, AI and new tech. His focus is on covering startups developing cutting-edge technology across emerging sectors such as Deep-Tech, AI among others.